from aff_poly_sig.exp_sig import expsig, withwords, expsig_withwords, momentsAffine and polynomial methods for signatures

Code for Laplace transform of the signature of a one dimensional Brownian motion and expected signature of a continuous polynomial process.

Documentation

The code documentation is available at https://sarasvaluto.github.io/AffPolySig/.

The original theoretical results can be found in the following papers.

C. Cuchiero, G. Gazzani, J. Möller, and S. Svaluto-Ferro. Joint calibration to SPX and VIX options with signature-based models. ArXiv e-prints, 2023. https://arxiv.org/abs/2301.13235.

C. Cuchiero, S. Svaluto-Ferro, and J. Teichmann. Signature SDEs from an affine and polynomial perspectiv. ArXiv e-prints, 2023. http://arxiv.org/abs/2302.01362

How to install

After cloning the repository, cd (change directory) to the repo and enter this into your terminal:

pip install -e .How to use

Expected signature and moments of a polynomial process

The goal of this code is to compute the expected signature \(\mathbb E[\mathbb X_T]\) of a polynomial process \(X\). In the one dimensional case it also provides an expression for its moments. As a first step import the following functions.

Next, define the parameters of the polynomial process of interest. Given the drift vector \[b(X_t)^i=b_i+\sum_{j=0}^db_{ij}X_t^j,\] and the diffusion matrix \[a(X_t)^{ij}=a_{ij}+\sum_{k=0}^da_{ijk}X_t^k+\sum_{k,h=0}^da_{ijkh}X_t^kX_t^h,\] we use the following parametrisation of the characteristics \[\begin{align*} b_{const}[i]&=b_i,& b_{lin}[i,j]&=b_{ij},\\ a_{const}[i,j]&=a_{ij},& a_{lin}[i,j,k]&=a_{ijk},& a_{quad}[i,j,k,h]=a_{ijkh}. \end{align*}\] Coefficients need then to be saved in a tuple as illustrated in the code below. Define also the initial condition \(x_0\).

For this example we consider a one dimensional Jacobi process without drift setting \(b(X_t)^0=0\) and \(a(X_t)^{00}=X_t^0(1-X_t)^0\). We set \(x_0=1/2\).

import numpy as np

#Dimension of the process

dim=1

#Coefficients of the characteristics

b_const=np.zeros(dim)

b_lin=np.zeros((dim,dim))

a_const=np.zeros((dim,dim))

a_lin=np.zeros((dim,dim,dim))

a_quad=np.zeros((dim,dim,dim,dim))

a_lin[0]=1

a_quad[0]=-1

coeff=(b_const,b_lin,a_const,a_lin,a_quad)

x0=np.zeros(dim)

x0[0]=1/2The last parameters to define are given by the lenght of the expected signature we would like to compute (len_max) and the time at which we would like to do it (T).

len_max=10

T=1To get the expected signature we can then use the function expsig.

expsig(coeff,x0,len_max,dim,T)array([1.00000000e+00, 0.00000000e+00, 7.90150699e-02, 0.00000000e+00,

1.45583443e-03, 0.00000000e+00, 1.14548260e-05, 0.00000000e+00,

4.94622744e-08, 0.00000000e+00, 1.34438690e-10])To obtain a better readable output one can use the function withwords.

E=expsig(coeff,x0,len_max,dim,T)

withwords(E,dim)[[1.0, []],

[0.07901506985356974, [0, 0]],

[0.0014558344297645905, [0, 0, 0, 0]],

[1.145482602482784e-05, [0, 0, 0, 0, 0, 0]],

[4.94622743536099e-08, [0, 0, 0, 0, 0, 0, 0, 0]],

[1.3443868989326117e-10, [0, 0, 0, 0, 0, 0, 0, 0, 0, 0]]]The same result can be obtained directly using expsig_withwords, which combines the two steps above.

expsig_withwords(coeff,x0,len_max,dim,T)[[1.0, []],

[0.07901506985356974, [0, 0]],

[0.0014558344297645905, [0, 0, 0, 0]],

[1.145482602482784e-05, [0, 0, 0, 0, 0, 0]],

[4.94622743536099e-08, [0, 0, 0, 0, 0, 0, 0, 0]],

[1.3443868989326117e-10, [0, 0, 0, 0, 0, 0, 0, 0, 0, 0]]]In one dimension (dim=1) we can also use the function moments to compute the moments of the process.

moments(coeff,x0,len_max,dim,T)array([1. , 0.5 , 0.40803014, 0.36204521, 0.33448524,

0.31613774, 0.30305083, 0.29324856, 0.28563369, 0.27954838,

0.2745743 ])Laplace transform in the Brownian setting

The goal of this code is to compute the Laplace transform \(\mathbb E[e^{\langle \mathbf u^{sig}, \mathbb X_t^{sig}\rangle}]\) and \(\mathbb E[e^{\langle \mathbf u^{pow}, \mathbb X_t^{pow}\rangle}]\), where \(X\) denotes a Brownian motion and \(\mathbb X^{sig}\) and \(\mathbb X^{pow}\) the corresponding extensions. Precisely, we consider the following two extensions: the signature \[\mathbb X_t^{sig}:=(1,X_t,\frac {X_t^2}2,\ldots),\] and the power sequence \[\mathbb X_t^{pow}:=(1,X_t,X_t^2,\ldots).\] As a first step import the following functions.

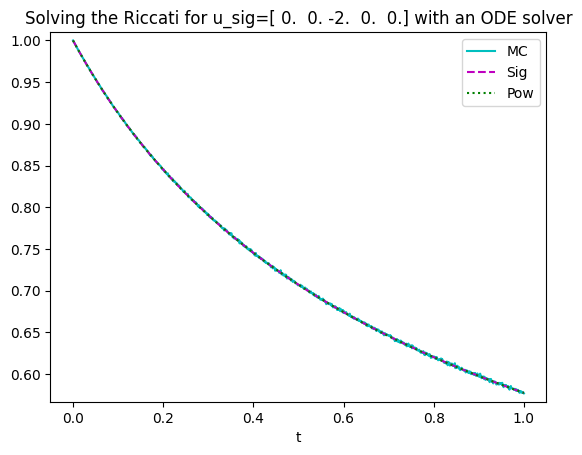

from aff_poly_sig.riccati_bm import appr_exp_sig, appr_exp_pow, MC, CoDNext, we introduce the parameters of interest. We in particular have T for the time horizon, K_u for the lenght of (the approximation of) \(\mathbf u^{sig}\) and \(\mathbf u^{pow}\), u_sig for \(\mathbf u^{sig}\) with the signature’s extension, and u_pow for \(\mathbf u^{pow}\) with the power sequence’s extension. As an example we compute \[\mathbb E[\exp(-2\frac{X_t^2}2)]=\mathbb E[\exp(-X_t^2)]\] for each \(t\in[0,T]\), where \(X\) denotes a Brownian Motion and \(T=1\). The corresponding parameters are given in the following cell.

import math

import matplotlib.pyplot as plt

T=1 # [0,T] time horizon

#u in terms of the sig lift

K_u=5

u_sig=np.zeros(K_u)

u_sig[2]=-2

#u in terms of the powers lift

u_pow=u_sig.copy()

for k in range(0,K_u):

u_pow[k]=u_pow[k]/math.factorial(k)One then just needs to fix the computational parameters, namely the grid for the computation of the signature (timegrid) and the trucation’s level K for the solution.

n_time=1000

timegrid = np.linspace(0,T,n_time)

K=30The desired Laplace transform can then be computed using appr_exp_sig and appr_exp_pow. The finals sig and pow denote the employed extensions.

L_sig=appr_exp_sig(u_sig,timegrid,K)

L_pow=appr_exp_pow(u_pow,timegrid,K)To test the results, one can compare them to the results obtained by a Monte Carlo approximation. That’s what the MC function does.

N=100000 # number of samples

n_MC=1000 # number of times ticks

MonteCarlo = MC(u_sig,T,n_MC,N)#Monte Carlo

#MonteCarlo_CoD = CoD(np.real(MonteCarlo),n_MC, n_time)

plt.plot(np.linspace(0,T,n_MC),MonteCarlo,'c',label='MC');

#Sig Lift

plt.plot(timegrid,L_sig,'m--',label='Sig');

#Pow Lift

plt.plot(timegrid,L_pow,'g:',label='Pow');

plt.ylim(min(MonteCarlo.real-0.01),max(MonteCarlo.real)+0.01)

plt.xlabel("t")

plt.title(f'Solving the Riccati for u_sig={u_sig.real} with an ODE solver')

plt.legend();